Letter #33 – ✍️ Writing in Seattle 🌲

This week’s newsletter:

It’s been a while

A near-death experience

Our finance updates

Automate, automate, automate

How much we invest monthly

Hi friends and fam, ♥️

It’s been a while!

We were all wrapped up in getting ready for our two-week Korea trip—and just like that, we were back and scrambling to get our lives together again 🫠. Jet lag definitely hits harder with age.

Seattle is also coming alive this time of year, with all the blooms 🌷 and sunshine. 🌞

We've been soaking it up—catching up with friends and neighbors, spending more time outdoors, and diving into hobbies. (Angie just finished her third painting of the year! 🧑🏻🎨)

On top of that, we’ve started a few small social projects. 🤭 It’s already a joy to see friends, but there’s something extra special about doing meaningful things together.

At Gamcheon Culture Village in Busan—you can even spot cherry blossoms 🌸 in the background. 👀 South Korea 🇰🇷 is an incredible travel destination. 💗 And the food still has us craving more to this day. 🤤

Now, back to our newsletter—

We met a woman on a tour of the Gyeongju Historic Areas in Korea, a cancer survivor who told us a wild story.

Eighteen years ago, she had a cardiac arrest and a near-death experience! 😱

She described floating above her body in the ER, watching everything unfold, then speaking with a being dressed in all white standing in the corner of the room.

She pleaded for more time—her youngest son, who has autism, still needed her. Somehow, she won the negotiation and came back with three messages from that being.

One of them?“Your husband is stealing you blind.”

Apparently, just before the cardiac arrest, her (now ex-) husband—who was also a lawyer—convinced her to sign paperwork under the pretense of transferring assets to their children. In reality, he funneled everything into his own name. 😰

We were stunned and asked how she felt about it after coming back.

She simply shrugged 🤷 and said:“Money gained, money lost. I can always make more. It doesn’t bother me.”

And that was the perspective of someone who’s come face-to-face with death.

May we all learn something from that kind of clarity. 🙏

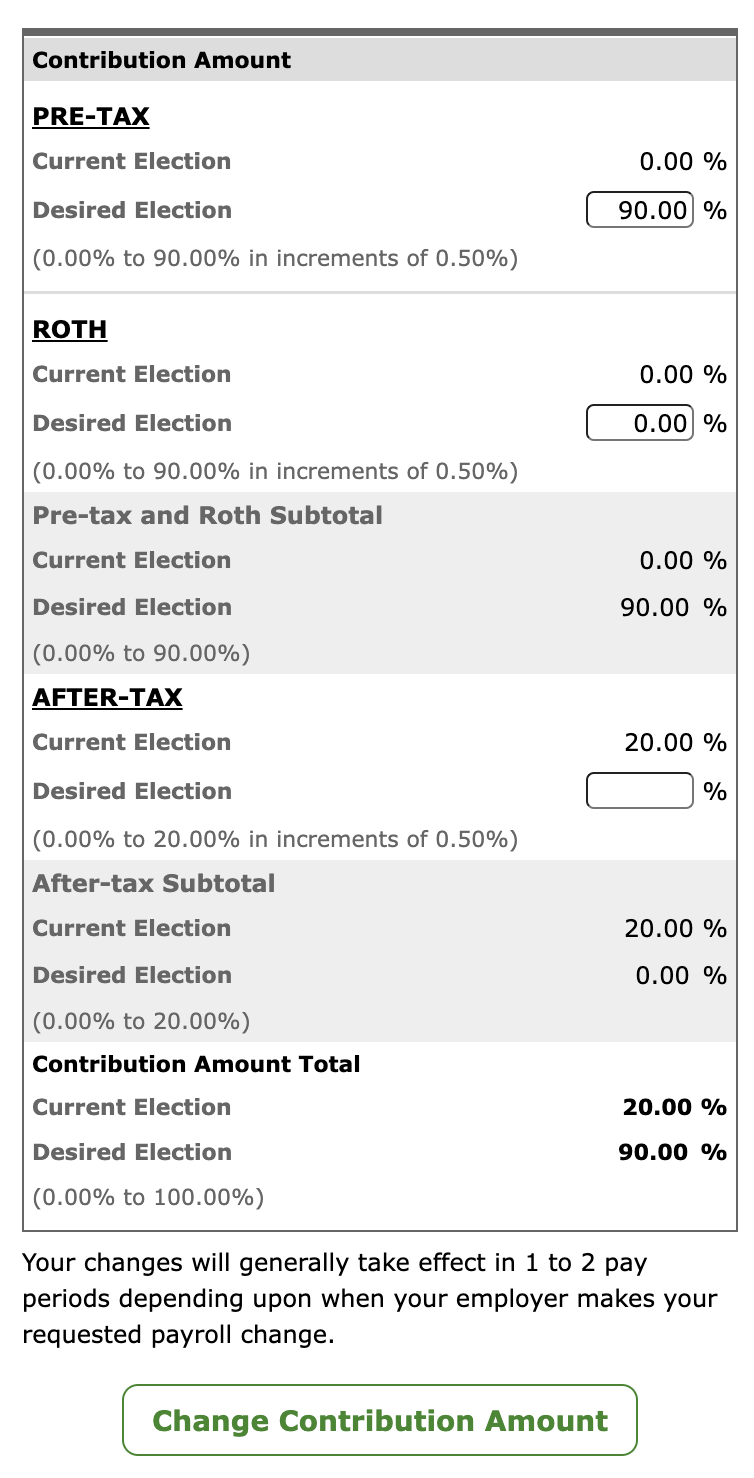

Jet lag didn’t fog our brains all day 😶🌫️—so in our more lucid moments, Angie sat down and gave our finances a little makeover.

Be lazy. Like, truly lazy. The couch potato kind. 🛋️🥔 That’s the goal. (Not convinced? Learn more here.)

So we leaned into that mindset and added more automation to our finances. 🤓

Automatically max out Mega Backdoor Roth 401(k) and HSA from our paychecks.

The rest went into checking.

Manually invest 40% of that leftover money.

Budget the rest.

Because we were manually investing that 40%, our emotions got involved. It wasn’t a “Monday at 10 AM, buy this index fund” kind of routine. It was more like, “Hmm… this price doesn’t look great today. 🧐 Maybe tomorrow.”And just like that, dollar-cost averaging (what’s this?)? Gone. 💨

Even worse, when we overspent, we’d dip into that investment money. 😅 Yep—delaying our financial freedom one impulse at a time.

Still maxing out Mega Backdoor Roth 401(k) and HSA—because tax advantages are gold. (why?)

But now, our post-tax paycheck is split automatically into two places:For example:40% of the paycheck (say, $1,000) is auto-deposited into the Fidelity account, ready to be invested.

Checking – every dollar gets budgeted.

Fidelity Brokerage – straight into the Settlement Fund.

In parallel, we’ve set up recurring investment with money from the Settlement Fund.For example: On Monday every two weeks, $500 → VOO, $300 → QQQM, $200 → individual stocks.Note: Recurring investments are fixed, but paycheck deposits to the Settlement Fund can vary slightly. We leave a small buffer in the Settlement Fund and check monthly to adjust if needed.

We’re no longer swayed by market noise or tempted to “wait for a dip.” 🙈

We also don’t accidentally spend investment money on impulsive buying. 🙃

It keeps us consistent and aligned with our values—choosing freedom over impulse. 🤌

Out of 100% of our income:

63.59% invested

29.13% stocks

7.28% crypto

23.75% retirement accounts

3.42% HSA

36.41% free to spend(includes monthly donations and support for Angie’s parents)

Your exact % will vary depending on comfort and risk tolerance.

Investing and saving should feel a bit like self-growth 🌱—it should hurt a little, but never be so painful that you give up.

For us, it’s really all about treading that balance.

🔮 Not sacrificing today’s joy for an uncertain future.

✋ Being intentionally frugal with things that don’t add value.

🫶 And spending freely on what matters: quality food (mostly organic—bananas get a pass), health, relationships, and meaningful experiences.

😔 And not into the YOLO mindset that keeps you stuck in a job you don’t love, just counting down to your next vacation.

Because life’s better when you enjoy every day, not just vacation days. ✨

(Only if you want to stop stressing about money 😉 and start building your freedom)

Automate your finances – 1 hour

Calculate your investment percentages – 2 hours

Hope it's helpful for your journey to Freedom 🙏

Love you to freedom and back, 🫰

Angie & Tyler

🥟 Crystal shrimp dumplings: Angie’s been obsessed with this the prawn hacao 🤤 — the texture is spot on. Perfect for a quick, easy, and delicious meal when you’re short on time.

🍚 Frozen rice: Even with a rice cooker, perfect rice can take up to an hour—unless you’re in a rush and use the quick-cook setting. But honestly, when we’re in the mood for rice, we rarely have the patience to wait that long. 😩So here’s our go-to trick:We cook a big batch of rice, let it cool, portion it into molds, and freeze it. Then whenever we want rice, we just pop a portion in the microwave—it tastes just like it was freshly made. Total game-changer. 🍚✨

Personal Finance 💵

Airbnb & VRBO hosting 🏘️

Travel 🧳✈️

Free • 5-min read

Our hard-earned lessons on financial freedom, Airbnb hosting, and living your best life. 🐶⚾️

The tea is ready to spill. 💦

Let’s stroll to Freedom together!

No fluff. Good vibes and honesty Only 🙏🏼